The US Digital Dollar Paper

Money and Payments: The US Digital Dollar in the Age of Digital Transformation

The FED has finally released the long awaited paper on the Digital Dollar, the US CBDC. The “discussion” paper released on Thursday Jan 20th is titled Money and Payments: The U.S. Dollar in the Age of Digital Transformation. The paper starts off by providing a clear definition of a CBDC stated by the central bank.

“CBDC is defined as a digital liability of a central bank that is widely available to the general public. In this respect, it is analogous to a digital form of paper money.”

Money And Payments

The focus on the paper covers the pros and cons of a US Digital Dollar and how it could serve as a complement to the current system. The paper largely has no concrete statement on whether or not the FED plans to move forward on a CBDC, however that question is more of a matter of when. The Board of Governors includes several statements and findings of the increased efficiency and effectiveness of a digital dollar. The CBDC must be privacy-protected, intermediated, widely transferable, and identity-verified.

The criteria for the CBDC are laid out clearly in the paper and are as follows:

The Digital Dollar will complement the current financial system and it’s developments

Safely and Securely Meet the Needs and Demands of Payment Services

Improve Cross Border Payments

Support the Dollar’s International Role

Improve Financial Inclusion + Extend Public Access to Central Bank Money

As well as the risks and concerns with launching a CBDC:

Changes to Financial-Sector Market Structure

Safety and Stability of the Financial System

Efficacy of Monetary Policy

Privacy and Data Prevention + Prevention of Financial Crimes

Operational Resilience and Cybersecurity

The objective of the discussion paper is to openly address the pros and cons of the current system and weight the pros and cons of adding a CBDC into it. They lay out what would be needed for integrating a CBDC into the system. The FED Board of Governors views the advancements in cryptocurrencies and other leading competitors as a threat and how a CBDC is looked at as an important aspect to the stability of the Dollar as the world’s reserve currency. The USD competitors aren’t only stablecoins and crypto, as 88 leading central banks are exploring or piloting CBDCs.

“The digital dollar may be a necessary defensive move.”

The Bahamas launched the Sand Dollar in October 2020 being the first nation to effectively launch a CBDC. They announced the project in 2016, the same year China announced they’re starting their project on a CBDC. The Central Bank of the Bahama’s statement on the CBDC is parallel to the common messages seen across the other central banks. They all say something along the lines of “ We want to remain competitive and reach out to those who are ‘unbanked’ in the world.”

“The main goals of the Sand Dollar are to modernize and streamline the country’s financial system, reduce service delivery costs, increase transactional efficiency and improve financial inclusion.”

Clearly it was a very massive step forward in the increasingly digital financial system. The Digital Cash/Electronic Payment (DC/EP) is so far a major success for China and a major threat to the US, why? International Trade. China and it’s leaders are urging large US companies operating in China to begin accepting the CBDC. Subway and McDonald’s already accept it.

The digital yuan is right now the leading CBDC from a large global central bank as they are in the stage of full scale use during the Olympics and will be nearing the close of the “pilot program”. The digital wallet app being used by citizens for the digital yuan has reached over 260 million downloads and is tracing the spending of all the users.

The scariest part is the programmability aspect to the wallet and the DC/EP has expirations, as well as the social credit system integrations. The monitoring and facial recognition software in China facilitates a lot of data and wallet users can incur penalties and fines within the wallet. Fail to pay your fine? It is automatically taken out, just like the IRS does in the US.

However, the large scale aspect are the number of large countries piloting their own CBDC and the US is the furthest behind.

France

Canada

Singapore

South Africa

UAE

Saudi Arabia

Uruguay

Ghana

Tunisia

Currently only The Bahamas and Nigeria have successfully launched and are actively using a CBDC.

Digital Assets

The FED is clearly examining new growth and challenges posed by cryptocurrencies, mostly stablecoins. The FED also recently just released a long paper on stablecoins titled Growth Potential and Impact on Banking.

Their closing remarks on stablecoins was “current usage of stablecoins is primarily driven by cryptocurrency trading, limited peer-to-peer payments, and DeFi. Looking forward, stablecoins may see further growth through their facilitation of more inclusive payments and financial systems.”

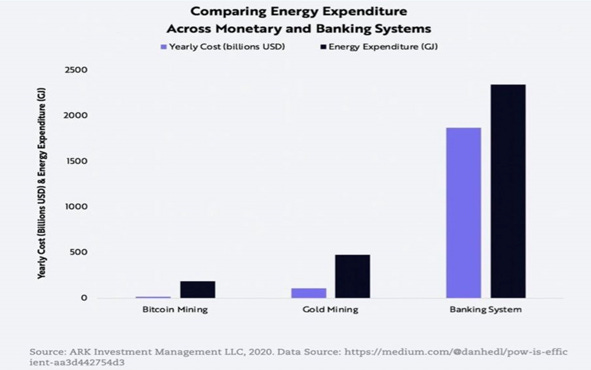

In the Money and Payments paper, the FED expressed regulatory concerns for stablecoins and asserting concerns with cryptocurrencies regarding their “energy footprint” which we all know is clearly overstated.

It is no secret that crypto has caused this response from the world’s central banks and governments. According to a report last year released by PwC over 60 central banks have been exploring CBDCs since 2014.

“While the existing U.S. payment system is generally effective and efficient, certain challenges

remain. In particular, a significant number of Americans currently lack access to digital banking

and payment services. Additionally, some payments—especially cross-border payments—remain

slow and costly

The FED sees a lot of potential in a CBDC, and rightfully so. The Digital Dollar Foundation that is partnering with Accenture and working with MIT are developing 5 different versions of a US CBDC. Accenture’s work in CBDCs also extends to Bank of Canada, the Monetary Authority of Singapore, the European Central Bank, and, most recently, Sweden’s Riksbank. As of July 2021, there were 88 countries around the world (making up ~ 90% of that global economy) were pursuing CBDC projects in many different stages.

For example, Sweden’s Riksbank is planning an electronic version of its official currency krona, called e-krona, to facilitate the development of an alternate payment system after a decline in the use of cash in the country.

Bitcoin, Ethereum, and other cryptocurrencies have posed a major threat to the incumbent financial system and have created a better form of money. These currencies are superior to fiat and are highly productive assets. People have begun to see this and the 2 largest cryptocurrencies has become household names at this point.

“The root problem with conventional currency is all the trust that’s required to make it work. The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust. Banks must be trusted to hold our money and transfer it electronically, but they lend it out in waves of credit bubbles with barely a fraction in reserve. We have to trust them with our privacy, trust them not to let identity thieves drain our accounts. Their massive overhead costs make micropayments impossible.”

Satoshi Nakamoto

If the US dollar is to remain the world’s primary reserve currency in the unfolding century, it cannot remain an analog instrument and unit of account for things increasingly denominated as digital tokens. It must itself become a digital tokenized currency that measures, supports, and transacts with the world’s digital tokenized things of value. (Accenture)

End Note: Buy Bitcoin

(Feb 2015)

Good writeup 😎